What Companies Should Know About the SEC Climate Disclosure Rule

The new U.S. Securities and Exchange Commission (SEC) climate disclosure rule will impact all public companies. Is your company ready to meet its non-financial ESG reporting needs?

After nearly two years and over 24,000 comments from a multitude of stakeholders, the SEC released its long-awaited ruling, The Enhancement and Standardization of Climate-Related Disclosures for Investors. The rules require public companies to include additional climate-related disclosures in their annual reports and audited financial statements, with the stated goal of providing investors with more complete and reliable information about the impacts of climate-related risks on a registrant's business strategy, results of operations, and financial condition. The rules will phase in from FY 2025 to FY 2033.

How are companies impacted by the SEC climate-related disclosure rules?

All domestic and foreign companies publicly listed in the U.S., regardless of sector and industry, are required to comply with the SEC climate-related disclosure rules. Large accelerated filers (over $700M float) and accelerated filers (between $75M and $700M float) must disclose Scope 1 and 2 emissions if they are material. They must also obtain a third-party attestation of any disclosed Scope 1 and 2 emissions. Scope 3 emissions are not required in the new rules for any issuers. More information about Scope 1, 2, and 3 emissions and attestation is detailed below.

- Scope 1: Covers emissions that the company produces directly (e.g., if the company has a vehicle fleet, the fuel combustion would be covered by Scope 1).

- Scope 2: Covers emissions that the company produces indirectly through energy that it buys (e.g., the emissions produced by electricity that the company purchases).

- Scope 3 (not required under the SEC rules): Covers all other emissions associated with the company’s value chain that are not covered by Scope 1 and 2 (e.g., emissions from waste generated during operations).

- Greenhouse Gas (GHG) Emissions Attestation: The attestation must be provided by an independent third party that meets the proposed definition of an expert with significant experience measuring, analyzing, reporting, or attesting to GHG emissions. It must be conducted pursuant to publicly available or widely used standards established by a body that published the framework for public comment.

In addition to Scope 1 and Scope 2 emissions disclosures (if material), companies must disclose material climate-related information around governance, strategy, risk management, and metrics and targets. These topics align with the Task Force on Climate-Related Financial Disclosures (TCFD) pillars and include qualitative and quantitative reporting requirements. The SEC’s stated rationale behind this design is that many public companies already use the TCFD’s voluntary framework and are familiar with its structure. The emissions reporting framework draws upon methodology developed by the GHG Protocol with definitions based on the terminology used in the TCFD.

In determining what climate-related information is material, the SEC points to longstanding Supreme Court precedent: a matter is material if a reasonable investor would consider its disclosure or omission important when making an investment or voting decision. Companies will need to consider the materiality of their climate-related risks, and assess whether their targets, goals, scenario analyses, transition plans, and use of carbon offsets or renewable energy credits are material.

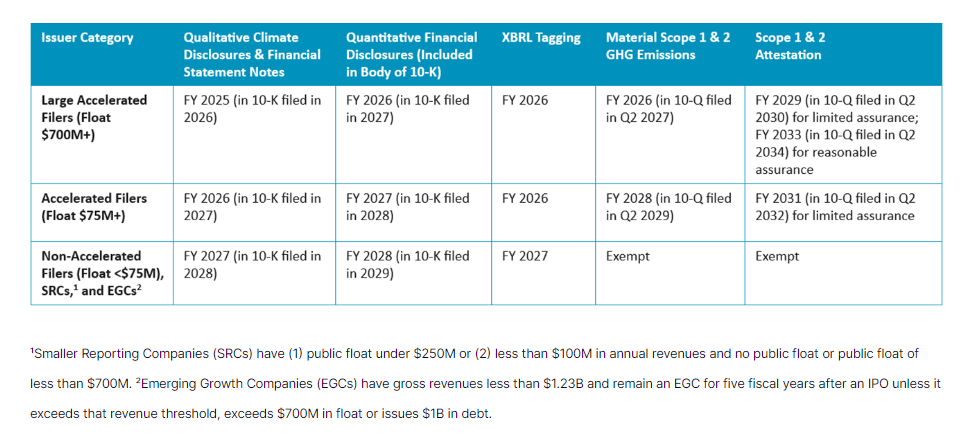

When do companies need to report climate-related disclosures?

(See table above)

What can companies do to prepare for the new reporting requirements?

Companies should familiarize themselves with the final rules and assess the potential impact on their business and financial statements. In addition to continuously monitoring and ensuring compliance with the evolving regulatory landscape, companies may consider the below actions to prepare:

- Conduct a gap analysis. A gap analysis helps compare your company’s current disclosures against the potential required disclosures and identify areas that your company is not currently reporting on. The TCFD framework is identified as a foundational structure and Nasdaq Sustainable Lens™ is a tool to help perform a gap analysis against standards.

- Map oversight responsibilities. Ensure your company has robust systems, controls, and procedures in place to support data collection, quality control, and reporting. In addition, engage with the board and management team to ensure effective governance and oversight of climate-related risks.

- Collect GHG data. Collect disaggregated GHG emissions data across all operations, based on the GHG Protocol, which provides the world’s most widely used GHG accounting standards for companies. Plus, obtain assurance over your GHG emissions disclosures to enhance the reliability and credibility of the information.

- Implement ESG data management software. With a platform like Nasdaq Metrio™, you can save time and organize complex ESG content and cross-referencing between the TCFD, Corporate Sustainability Reporting Directive (CSRD), Carbon Disclosure Project (CDP), Global Reporting Initiative (GRI), International Sustainability Standards Board (ISSB), and dozens of other voluntary and regulatory standards.

Nasdaq’s ESG offerings are well positioned to support the new framework. Nasdaq has full ESG lifecycle support for clients, including Nasdaq ESG Advisory for expert guidance on strategy, Nasdaq Metrio™ to support end-to-end sustainability data management, reporting, and disclosure, and Nasdaq Sustainable Lens™ to help benchmark data against peers and perform gap analyses against standards.

To find out how Nasdaq can best support your company with tools and insights throughout its ESG journey, get in touch here.